Premiums for ObamaCare-eligible health insurance plans are soaring this year, according to an analysis by the Urban Institute.

The study, sponsored by the Robert Wood Johnson Foundation, found that the lowest priced of the so-called gold plans that cover 80 percent of medical expenses for a 40-year-old non-smoker increased 19 percent nationally this year and 25 percent in Nevada. The lowest cost silver plans for that individual, which covers 70 percent of medical costs, went up 32 percent nationally and 45.6 percent in Nevada. The second lowest priced silver plans jumped 34.3 percent nationally and 48.3 percent in Nevada.

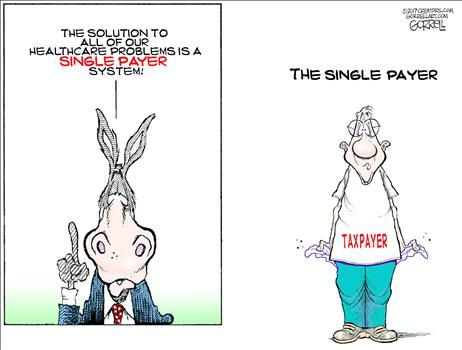

But not to worry, the Nevada Appeal newspaper in Carson City reports that more than 85 percent of the nearly 100,000 Nevadans who are covered by such plans through the Silver State Health Insurance Exchange will not pay much if any of that premium increase because they receive federal subsidies. Guess who pays those federal subsidies? All of us.

The Appeal reports that, according to a recent report by the Congressional Budget Office, the nationwide increase in premiums will cost the taxpayers $10 billion more in subsidies this year.

Of course, a state health exchange executive blamed the premium spikes on “instability in the health insurance market — much of it caused by tactics designed to undermine the Affordable Care Act. That includes the decision to stop paying insurance companies for the Cost Sharing Reduction subsidies mandated by the ACA for consumers making between 138 and 250 percent of the poverty level,” the Appeal explained.

The taxpayers get stuck with the bill either way — subsidize the insurer or subsidize the rate payer. Six of one, a half dozen of the other.

During the debate this past year over those Cost Sharing Reduction subsidies, The Wall Street Journal reported, “In an ironic twist, stopping the subsidies would also wind up costing the federal government more in the end, the (Congressional Budget Office) report said. Higher premiums for mid-priced plans would require the government to pay larger tax credits to consumers to help offset coverage costs. The federal deficit would increase by $194 billion through 2026, the report said.” Instead of paying $7 billion in subsidies to insurers, we are paying $10 billion to ratepayers.

Pay no heed to the fact ObamaCare premiums have been rising sharply since the law was passed in 2010 without a single Republican vote and using dirty tricks devised by Nevada’s own Sen. Harry Reid. According to the website eHealth, from 2013, the year before ObamaCare went into effect, through 2017, health insurance premiums had already increased 140 percent. Forget repeal and replace, just repeal. Remember at the ballot box this fall just who brought us this expensive boondoggle and would vote to keep it.

A version of this editorial appeared this week in some of the Battle Born Media newspapers — The Ely Times, the Mesquite Local News, the Mineral County Independent-News, the Eureka Sentinel, Sparks Tribune and the Lincoln County Record.